All Categories

Featured

Table of Contents

Life insurance isn’t just a policy; it’s a powerful way to secure your family’s financial stability. From protecting your loved ones from unexpected costs to planning for the future, the right life insurance policy ensures peace of mind. Term life insurance is a popular choice for those seeking temporary, cost-effective coverage, while whole life insurance provides lifelong protection and cash value growth. Universal life insurance is another flexible option, ideal for families and individuals looking to balance affordability with long-term financial goals.

For specific needs, final expense insurance ensures funeral costs are covered, and mortgage protection life insurance provides reassurance that your family can stay in their home. Accidental death insurance adds another layer of security for unique situations. Many of these policies also include living benefits, allowing policyholders to access funds during critical times, such as illness or emergencies.

Life insurance isn’t just about protecting your loved ones; it’s also a strategic tool for building a solid financial foundation. quick approval life insurance policies through agents. Speak with a licensed insurance agent today to explore policies designed for your specific needs, whether you’re planning for retirement, saving for college, or securing your family’s future. Request a free quote now to start building a secure tomorrow

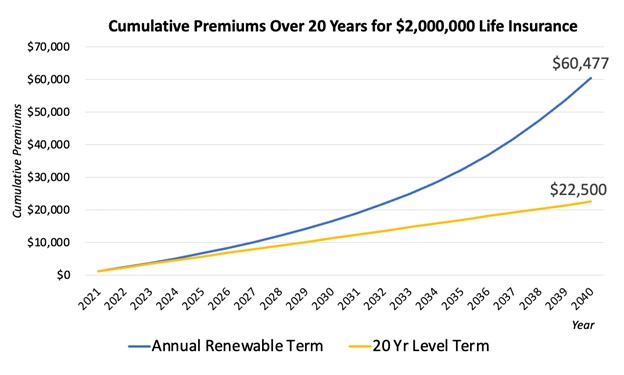

They commonly provide an amount of insurance coverage for much less than long-term types of life insurance. Like any type of plan, term life insurance policy has advantages and drawbacks depending upon what will function best for you. The advantages of term life consist of affordability and the ability to tailor your term size and coverage amount based upon your needs.

Depending on the kind of plan, term life can offer fixed costs for the entire term or life insurance on degree terms. The death benefits can be taken care of.

Term Life Insurance With Accelerated Death Benefit

You ought to consult your tax obligation consultants for your specific accurate situation. Fees reflect plans in the Preferred Plus Rate Course concerns by American General 5 Stars My agent was really experienced and handy in the procedure. No pressure to buy and the procedure fasted. July 13, 2023 5 Stars I was satisfied that all my needs were fulfilled immediately and skillfully by all the representatives I spoke with.

All documentation was electronically completed with accessibility to downloading and install for individual documents upkeep. June 19, 2023 The endorsements/testimonials presented need to not be construed as a referral to purchase, or an indicator of the worth of any type of services or product. The endorsements are actual Corebridge Direct customers who are not affiliated with Corebridge Direct and were not given settlement.

1 Life Insurance Policy Data, Information And Market Trends 2024. 2 Cost of insurance policy rates are identified making use of techniques that vary by firm. These rates can vary and will usually boost with age. Prices for energetic workers might be different than those readily available to ended or retired employees. It is essential to check out all elements when assessing the general competition of prices and the value of life insurance policy coverage.

Best Does Term Life Insurance Cover Accidental Death

Nothing in these materials is intended to be advice for a certain scenario or individual. Please consult with your very own consultants for such advice. Like many group insurance coverage policies, insurance policy plans supplied by MetLife consist of particular exemptions, exceptions, waiting periods, reductions, restrictions and terms for maintaining them in pressure. Please contact your benefits manager or MetLife for prices and total information.

For the many component, there are 2 kinds of life insurance policy plans - either term or permanent plans or some combination of the two. Life insurance providers provide numerous forms of term plans and conventional life policies along with "passion delicate" items which have actually ended up being a lot more widespread because the 1980's.

Term insurance policy offers protection for a specified time period. This period might be as short as one year or provide protection for a particular number of years such as 5, 10, twenty years or to a defined age such as 80 or sometimes as much as the oldest age in the life insurance mortality tables.

Guaranteed The Combination Of Whole Life And Term Insurance Is Referred To As A Family Income Policy

Currently term insurance coverage rates are really affordable and among the most affordable historically experienced. It needs to be kept in mind that it is a widely held belief that term insurance coverage is the least expensive pure life insurance policy coverage available. One requires to examine the policy terms thoroughly to make a decision which term life choices appropriate to fulfill your specific conditions.

With each new term the premium is boosted. The right to renew the policy without proof of insurability is an essential advantage to you. Or else, the threat you take is that your health and wellness may weaken and you might be unable to get a plan at the same prices or even in any way, leaving you and your recipients without insurance coverage.

You need to exercise this choice during the conversion duration. The size of the conversion period will certainly vary depending upon the kind of term policy bought. If you transform within the prescribed period, you are not needed to provide any type of info regarding your wellness. The costs price you pay on conversion is usually based on your "present achieved age", which is your age on the conversion day.

Under a level term policy the face amount of the policy remains the same for the entire duration. Often such policies are sold as home mortgage protection with the quantity of insurance coverage decreasing as the equilibrium of the mortgage lowers.

Typically, insurance companies have not can change costs after the plan is offered (voluntary term life insurance). Considering that such policies may continue for numerous years, insurance firms should make use of conventional death, interest and expenditure price price quotes in the costs computation. Flexible premium insurance, however, permits insurers to provide insurance coverage at reduced "existing" costs based upon much less conventional assumptions with the right to change these premiums in the future

Honest Guaranteed Issue Term Life Insurance

While term insurance is made to give protection for a specified amount of time, long-term insurance policy is developed to provide protection for your entire lifetime. To keep the costs price degree, the premium at the more youthful ages exceeds the actual cost of protection. This added premium builds a reserve (cash value) which helps pay for the plan in later years as the price of security rises above the costs.

Under some plans, costs are needed to be spent for a set number of years. Under other plans, costs are paid throughout the policyholder's lifetime. The insurer spends the excess costs bucks This kind of plan, which is in some cases called money value life insurance policy, creates a cost savings aspect. Cash values are important to an irreversible life insurance coverage policy.

Level Term Life Insurance

Occasionally, there is no relationship in between the size of the cash money worth and the premiums paid. It is the money worth of the policy that can be accessed while the policyholder is to life. The Commissioners 1980 Requirement Ordinary Death Table (CSO) is the current table made use of in computing minimal nonforfeiture values and plan gets for regular life insurance policy policies.

Lots of irreversible policies will have arrangements, which define these tax obligation needs. There are 2 standard classifications of long-term insurance policy, standard and interest-sensitive, each with a variety of variants. Additionally, each category is usually available in either fixed-dollar or variable form. Traditional entire life plans are based upon long-term estimates of expense, interest and mortality.

If these estimates transform in later years, the business will certainly change the costs appropriately yet never over the maximum guaranteed costs specified in the plan. An economatic entire life policy provides for a standard quantity of taking part whole life insurance policy with an extra supplemental coverage given through making use of returns.

Because the premiums are paid over a much shorter span of time, the costs settlements will certainly be greater than under the entire life strategy. Single premium entire life is limited payment life where one large superior repayment is made. The plan is totally compensated and no additional premiums are called for.

{kind=link}

Latest Posts

How To Sell Final Expense Insurance

Death Burial Insurance

Funeral Cover Up To 85 Years