All Categories

Featured

Table of Contents

Policies can also last until specified ages, which in the majority of instances are 65. Past this surface-level info, having a higher understanding of what these strategies require will certainly help guarantee you acquire a plan that fulfills your requirements.

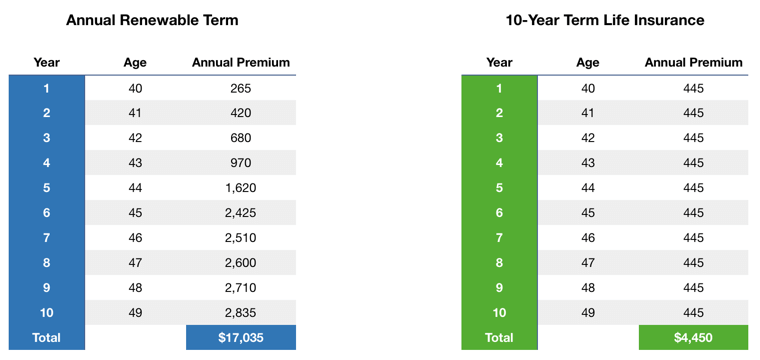

Be conscious that the term you pick will certainly influence the costs you pay for the policy. A 10-year level term life insurance policy policy will set you back less than a 30-year plan because there's less possibility of an event while the strategy is active. Lower danger for the insurance company relates to lower premiums for the policyholder.

Your household's age need to additionally affect your plan term selection. If you have young kids, a longer term makes sense due to the fact that it protects them for a longer time. If your children are near their adult years and will certainly be economically independent in the near future, a much shorter term could be a better fit for you than an extensive one.

Nonetheless, when comparing entire life insurance coverage vs. term life insurance policy, it deserves keeping in mind that the last typically sets you back much less than the former. The outcome is extra coverage with lower premiums, giving the most effective of both globes if you need a significant quantity of insurance coverage however can not manage an extra pricey policy.

What is Level Term Life Insurance Meaning? Learn the Basics?

A degree fatality benefit for a term plan usually pays as a swelling amount. When that occurs, your beneficiaries will get the entire quantity in a solitary repayment, and that quantity is ruled out earnings by the internal revenue service. For that reason, those life insurance policy profits aren't taxable. Some level term life insurance policy firms allow fixed-period settlements.

Interest payments received from life insurance policy plans are considered income and undergo taxation. When your level term life policy ends, a couple of different things can take place. Some coverage terminates instantly without any option for renewal. In other circumstances, you can pay to extend the plan beyond its initial day or transform it into an irreversible policy.

The downside is that your sustainable level term life insurance will certainly come with greater premiums after its initial expiry. Advertisements by Cash.

Life insurance companies have a formula for computing risk making use of mortality and interest (Level term vs decreasing term life insurance). Insurance companies have thousands of clients obtaining term life policies simultaneously and make use of the premiums from its energetic policies to pay surviving beneficiaries of other policies. These firms utilize mortality tables to approximate just how lots of people within a details group will file death insurance claims each year, and that info is made use of to determine average life span for prospective policyholders

Furthermore, insurance policy companies can invest the cash they receive from costs and raise their revenue. The insurance coverage company can invest the money and gain returns.

The following area information the benefits and drawbacks of level term life insurance coverage. Predictable costs and life insurance coverage Simplified policy framework Potential for conversion to permanent life insurance Limited insurance coverage duration No money value buildup Life insurance policy premiums can raise after the term You'll discover clear advantages when comparing level term life insurance policy to other insurance types.

How Does Level Benefit Term Life Insurance Compare to Other Types?

From the minute you take out a plan, your costs will certainly never ever alter, aiding you plan monetarily. Your insurance coverage will not differ either, making these plans effective for estate preparation.

If you go this course, your premiums will certainly boost however it's constantly great to have some adaptability if you desire to maintain an energetic life insurance coverage policy. Sustainable level term life insurance policy is another option worth considering. These plans permit you to maintain your existing strategy after expiration, giving versatility in the future.

What is 20-year Level Term Life Insurance? Discover the Facts?

You'll pick an insurance coverage term with the best level term life insurance coverage prices, but you'll no longer have coverage once the plan ends. This drawback can leave you clambering to discover a new life insurance policy in your later years, or paying a costs to extend your present one.

Numerous whole, global and variable life insurance coverage plans have a money value component. With among those plans, the insurance firm transfers a section of your monthly premium repayments right into a cash worth account. This account makes interest or is invested, assisting it grow and provide a much more significant payment for your beneficiaries.

With a degree term life insurance coverage policy, this is not the instance as there is no cash worth component. Because of this, your plan won't grow, and your fatality advantage will certainly never boost, consequently restricting the payout your beneficiaries will get. If you want a plan that offers a death advantage and constructs money value, explore entire, universal or variable plans.

The second your policy runs out, you'll no much longer have life insurance protection. It's frequently feasible to restore your policy, however you'll likely see your costs raise significantly. This can provide problems for retired people on a set income because it's an added cost they may not have the ability to afford. Level term and reducing life insurance policy offer similar policies, with the major difference being the death benefit.

Navigating life insurance options can be overwhelming, especially with so many policies available. This is where working with an experienced insurance broker or agent makes all the difference. Unlike insurance agents tied to a single provider, brokers offer access to multiple life insurance options, helping you find the most suitable policy for your needs - life insurance for college savings with agents. Whether it’s term life insurance for temporary coverage, whole life insurance for lifelong protection, or universal life for long-term growth, an insurance broker evaluates your unique goals and compares providers to secure the best coverage at competitive rates

For families, policies like final expense insurance, mortgage protection, and accidental death coverage offer tailored solutions to protect loved ones. Business owners can also benefit from key person insurance, ensuring continuity in the event of an unforeseen loss. With life insurance policies offering living benefits or instant coverage, brokers simplify the decision-making process and ensure your financial priorities are met.

By choosing the right insurance broker, you gain expert guidance, access to personalized recommendations, and the confidence of knowing your family or business is secure. Contact an insurance broker today to explore tailored life insurance options and secure peace of mind for the future.

It's a kind of cover you have for a specific amount of time, referred to as term life insurance policy. If you were to die throughout the time you're covered for (the term), your enjoyed ones obtain a fixed payout concurred when you secure the policy. You just pick the term and the cover quantity which you might base, for instance, on the cost of increasing children till they leave home and you might make use of the payment towards: Assisting to repay your mortgage, financial obligations, bank card or finances Aiding to pay for your funeral expenses Aiding to pay college fees or wedding event prices for your youngsters Assisting to pay living expenses, replacing your income.

All About Decreasing Term Life Insurance Coverage

The plan has no cash value so if your payments stop, so does your cover. If you take out a degree term life insurance policy you could: Select a dealt with amount of 250,000 over a 25-year term.

{kind=link}

Latest Posts

How To Sell Final Expense Insurance

Death Burial Insurance

Funeral Cover Up To 85 Years